Learn how high medication costs, inhaler prices, and insurance coverage gaps affect COPD/Asthma patients.

Living with a chronic disease management condition like Chronic Obstructive Pulmonary Disease (COPD) or asthma means grappling with a pervasive, and often overwhelming, financial stress. The necessity of constant care turns the simple act of breathing into a significant economic challenge for millions. This extensive financial toll, often referred to as "the cost of breathing," extends far beyond simple doctor visits; it encompasses the staggering medication costs, highly variable inhaler prices, complexities of insurance coverage, and the indirect expenses that can dismantle a family’s financial stability.

The Alarming Reality of Respiratory Disease Costs

The sheer scale of the financial burden imposed by COPD and asthma is immense, both globally and at the individual level. These diseases are among the most costly medical conditions. In the U.S., for example, the total annual medical expenditures for these conditions are substantial. For patients, the cost is often measured not just in dollars, but in missed workdays, lost productivity, and, critically, non-adherence to essential treatment plans due to cost.

A key factor driving the high expense is the reliance on specialized, often brand-name, inhaled therapies.

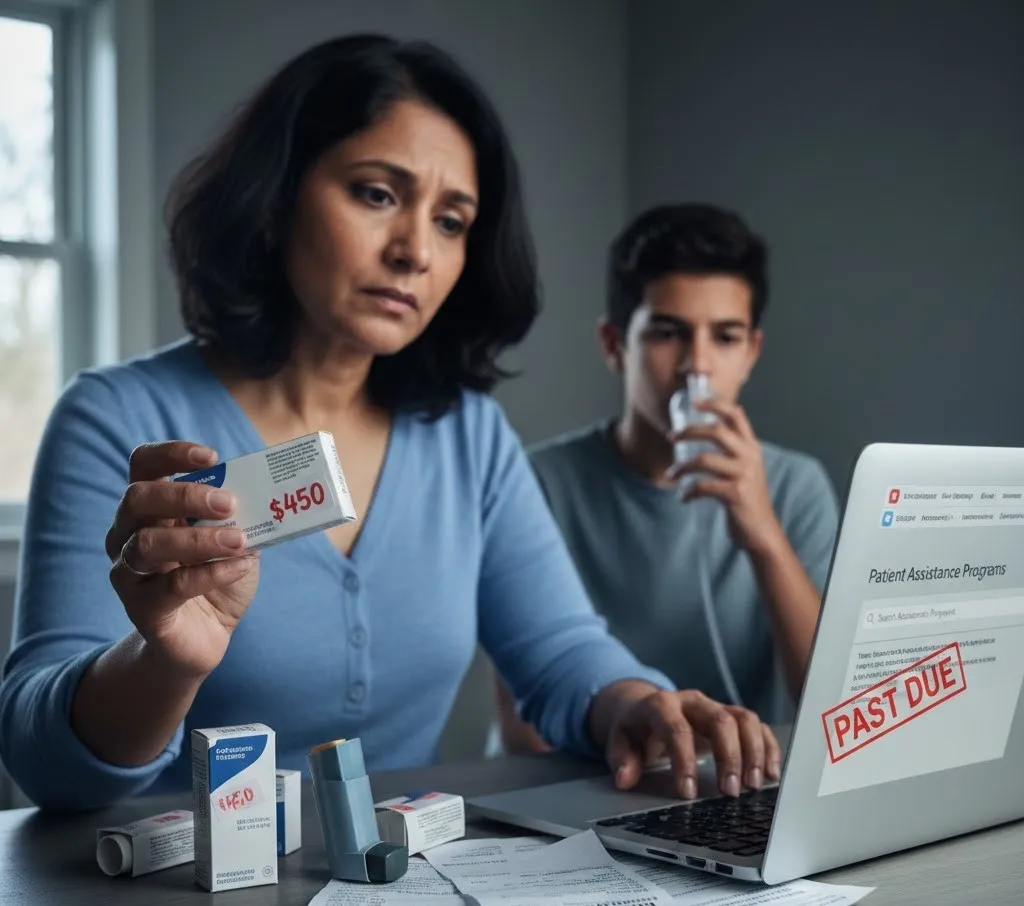

Medication Costs and Inhaler Prices

The core of effective asthma and COPD treatment involves daily maintenance medication, primarily delivered through inhalers. These devices administer a precise dose of medicine directly to the lungs, reducing inflammation and opening airways. However, the price tag for these life-sustaining devices is frequently exorbitant, especially for controller inhalers which are the cornerstone of long-term management.

- Controller Medications: These inhalers, which often contain inhaled corticosteroids (ICS) and/or long-acting bronchodilators (LABA/LAMA), are used daily to prevent symptoms and reduce exacerbations. They are significantly more expensive than reliever inhalers, often costing hundreds of dollars per device.

- Reliever Medications (e.g., Albuterol): While generally less expensive, even these essential "rescue" inhalers can have high retail prices, and frequent use (a sign of poorly controlled disease) rapidly multiplies the financial outlay.

- Brand vs. Generic: While generics exist for some oral medications, many of the newest and most effective inhaled combination therapies remain under patent, leading to artificially high prices that offer no generic equivalent.

This disparity in inhaler prices often forces patients to make difficult choices, a phenomenon known as cost-related medication nonadherence (CRN). Studies show that a significant percentage of adults with COPD, for instance, miss doses, take less than prescribed, or delay filling prescriptions just to save money. This cost-saving measure is counterproductive, as nonadherence leads to poorer disease control, which in turn dramatically increases the risk of costly emergency room visits and hospitalizations—the most expensive types of medical events.

The Maze of Insurance Coverage and Out-of-Pocket Maxima

Even with insurance coverage, patients face substantial out-of-pocket costs due to complex plan designs. The perception that a person with health insurance is financially protected is often shattered when they encounter the reality of high-deductible health plans and complex formularies.

- High Deductibles: Patients must pay 100% of their medical and prescription costs until their deductible is met. For expensive respiratory drugs, this can mean paying the full retail price for the first few inhalers of the year, quickly consuming a substantial portion of a family’s budget.

- Formulary Tiers: Medications are placed on different tiers, with Tier 3 and Tier 4 drugs (where many brand-name, specialized inhalers reside) requiring the highest copayments or co-insurance percentages.

- Coverage Gaps (e.g., Medicare Part D "Donut Hole"): Older adults on Medicare Part D can face a "coverage gap" where they are responsible for a large percentage of their drug costs after initial coverage limits are reached, until they reach catastrophic coverage. This gap can lead to severe financial stress and non-adherence among seniors.

The complexity of navigating these plans often leaves patients confused, leading to unanticipated costs and further economic hardship. The combination of high retail drug prices and restrictive insurance coverage creates a perfect storm of financial vulnerability.

Beyond the Prescription: The Total Financial Stress

The cost of breathing encompasses more than just medication. It includes a host of direct and indirect expenses that erode economic stability:

| Category | Direct Financial Costs | Indirect Financial Costs |

| Healthcare | Specialist co-pays, hospital stays, emergency room visits for exacerbations, oxygen therapy equipment, home health services. | Lost wages/productivity due to illness, caregiver expenses (time off work for family members), transportation costs to appointments. |

| Medication | Deductibles, copayments, co-insurance, full retail cost for uninsured/underinsured, auxiliary devices (spacers, nebulizers). | Reduced quality of life, increased mental health costs associated with financial stress. |

The immense financial burden creates a cycle where financial limitations lead to poor chronic disease management (non-adherence), which results in more severe exacerbations, requiring expensive emergency interventions, which restarts the cycle. Breaking this cycle is the goal of patient advocacy and assistance programs.

Finding Relief: Patient Resources and Patient Advocacy

For patients struggling with the high out-of-pocket cost of breathing, relief is often available through various financial assistance programs. These programs, frequently championed by patient advocacy groups, offer pathways to affordability for those who qualify.

Consumer-Focused Video Content: Assistance Tips

A consumer-focused video designed to address the high out-of-pocket cost of essential respiratory medications would provide vital, actionable tips. It would ideally explain that while inhaler prices are high, most patients do not have to pay the full list price.

Key segments of the video would include:

- Understanding Your Drug Tiers: A clear explanation of how insurance coverage and drug formularies affect co-pays. The video would urge patients to check their specific plan's formulary before getting a prescription filled.

- Exploring Manufacturer Co-Pay Cards and Coupons: Many pharmaceutical companies offer co-pay savings programs for commercially insured patients. These can reduce a monthly co-pay to as little as $0 or $35. Crucially, the video must warn that federal programs like Medicare and Medicaid are usually excluded.

- The Lifeline of Patient Assistance Programs (PAPs): This segment is the heart of the relief. PAPs, often run by the drug manufacturers themselves, are designed to provide free or heavily discounted medication to low-income, uninsured, or underinsured patients who meet specific financial and medical criteria.

- Actionable Tip: The video would direct viewers to online resources like the Medicine Assistance Tool (MAT) or RxAssist, which act as centralized search engines to find PAPs for specific drugs.

- Process Overview: It would explain the general application process: needing a doctor's signature, proof of income, and proof of non-coverage or financial hardship.

- Charitable Foundations: Highlighting independent non-profit organizations (e.g., HealthWell Foundation, Patient Access Network (PAN) Foundation) that offer grants to cover medication co-pays, deductibles, and insurance premiums for specific disease funds, including asthma and COPD.

- Generic/Discount Programs: Recommending generic equivalents (where available) and using pharmacy discount cards/programs (like SingleCare or GoodRx) for medications that may still be expensive even with insurance.

This educational approach empowers the patient to transition from a feeling of helplessness and financial stress to proactive patient advocacy for their own financial health.